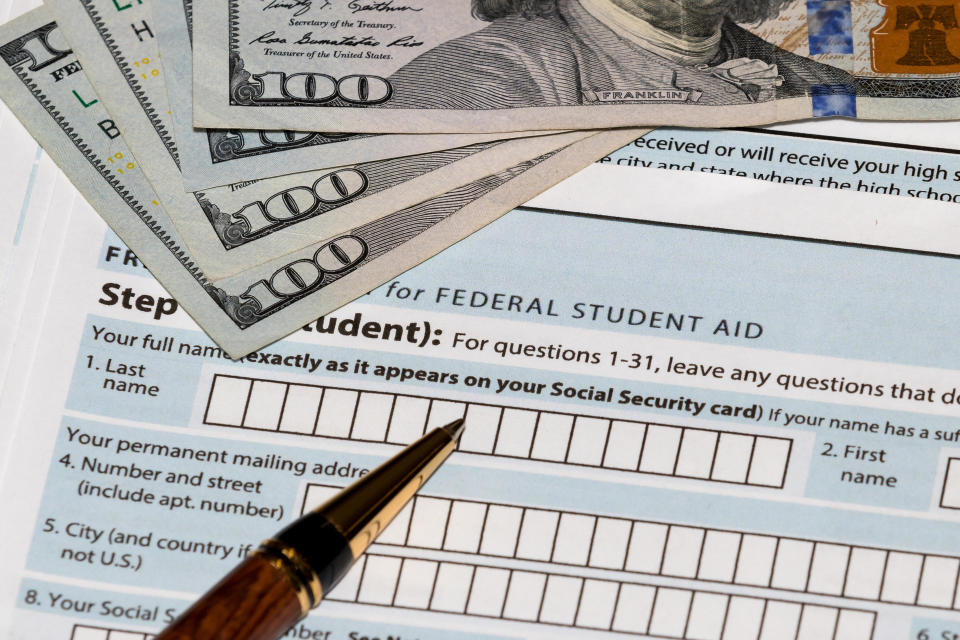

The future of student loan debt for millions of Americans hangs in limbo.

The Supreme Court will hear arguments in February to decide whether the Biden administration went beyond its authority with its agenda to eliminate billions of dollars in student debt.

Have Any $200 Quarters Lying Around? It’s Worth Checking Your Spare Change

Discover: 10 Things To Stop Buying in 2023

Under the new plan, nearly 26 million borrowers have applied to have some of their student loan debt erased, and the government has approved 16 million applications — but no debt has yet been canceled and the Education Department has put a halt on accepting applications.

So what should those with student loan debt be doing at the same time?

Understand Your Loans

“The most important things to understand are all aspects of your loan, including the terms and conditions, repayment options and potential consequences of default,” said Andrew Lokenauth, founder of Fluent in Finance. “Understanding your student loans and taking proactive steps to manage them can help you avoid financial troubles.”

Take Our Poll: Do You Think Student Loan Debt Should Be Forgiven?

Don’t Worry About Repaying Most Federal Loans (Yet)

“Payments for most federal students are currently suspended, and no interest is being charged while the suspension remains in place,” said Danny Cieniewicz, CFP, Hyperion Financial. “The suspension will likely remain in place until the current litigation involving the forgiveness plan issued by President Biden is resolved or if the forgiveness is implemented. Payments should resume 60 days after the action is announced, assuming no further action by the Department of Education.”

Note the Recently Passed SECURE Act 2.0

“In late December 2022, as part of the year-end omnibus spending bill, President Biden signed into law the SECURE Act 2.0, which will allow employers to match the amount an employee pays toward their student loans with a tax-advantaged contribution to their 401(k) or 403(b) retirement plan,” said Laurel Taylor, CEO and founder of Candidly. “This change revolutionizes the retirement savings opportunity for a generation of college graduates who have been saddled with student loan debt. If you’re an employee with student loan payments, you should approach your HR leaders and managers to ask them how they will enable you to get started.

“College graduates with student loan debt at the age of 30 have half of the retirement savings of those without student debt, on average,” Taylor said. “Nearly three-quarters of student loan borrowers say they are putting off maximizing their retirement savings until their student loans are paid off. This is transformational bipartisan legislation that empowers people to make simultaneous progress on paying down debt and building retirement savings earlier than ever before.”

Interest Loans Will Soar on Direct Loans

“While the current payment pause is in effect for direct loans, once the payment freeze ends, undergrad students will have an interest rate of 4.99% for any loan that was taken between July 1, 2022, and July 1, 2023,” Cieniewicz said . “For any PLUS loans — typically taken out by parents — the interest rate is 7.54%. For graduate students, the interest rate will be 6.54%.”

Start saving to pay down this interest now.

Repay Loans Now, if You Can

“I recommend that student loan holders continue making their required monthly payments until those student loans are forgiven or paid off,” said Andrew Griffith, associate professor of accounting at the LaPenta School of Business of Iona University. “Being in a default status or behind on these payments for any debts can have adverse consequences for a debtor when seeking a new job or needing to acquire additional credit — eg, denial of new credit, higher interest rates and charged fees, etc.

“Waiting for a government program to act and forgive debt can take a long time, and a borrower can experience negative financial consequences while waiting for this to happen.”

Look Into Refinancing Your Student Loans

“Refinancing your student loans may allow you to reduce your interest rate and monthly payments, and potentially save you money on interest over the life of the loan,” said Bill Morgan from Edvolt.com.

Don’t Apply for Debt Relief From the Government

As previously noted, the Department of Education has already approved 16 million applications for debt relief, but no debt has been canceled because of legal challenges. Additionally, applications for debt forgiveness are not being accepted at this time.

Look for Other Loan Repayment Options

“In certain circumstances, some foundations and nonprofit organizations have student loan repayment programs in place for those who qualify,” Griffith said. “Typically, these are directed at people who are working in critical roles — eg, healthcare — and doing this at below-market wages. Expect any payments made towards student loans by these types of organizations to be taxable income.”

More From GOBankingRates

This article originally appeared on GOBankingRates.com: Student Loan Updates: Everything To Know in January if You Have Debt